Canada’s pension system may be one of the strongest in the world, but the numbers tell a different story for women. Women are still only receiving 83 cents for every dollar men receive in retirement. A new report published by Ontario’s Pay Equity Office reveals this inequality hasn’t changed much since 1976, leaving many women financially vulnerable in their golden years. Retirement should be a time of security, but women in Canada are still coming up short because the gender pension gap has barely budged in almost 50 years.

A Closer Look at the Gender Pension Gap

The gender pension gap refers to the difference in retirement income between men and women. In Canada, this income comes from three main sources: Old Age Security (OAS) along with the Guaranteed Income Supplement (GIS), the Canada Pension Plan (CPP) or Québec Pension Plan (QPP), and private retirement savings plans. As of 2021, the GPG stood at 17%, meaning that Canadian women receive about $36,700 annually in retirement income on average, compared to men’s $44,000. This gap persists despite women’s increased participation in the workforce and is reflective of broader systemic inequities in both pay and employment. The gender pension gap does not impact all women equally; the effects of this gap are particularly pronounced for older women. In 2020, approximately 200,000 more women than men aged 65 and older were living below the low-income cut-off. Among women aged 75 and over, 21% had incomes below this threshold—51% higher than men in the same age group.

Intersectionality also plays a critical role in deepening the disparity. Factors such as race, disability, and immigration status intersect with gender to exacerbate the financial inequalities

women face in retirement. Racialized women, for example, tend to earn lower wages throughout their careers, leading to smaller pensions. Women with disabilities often face barriers to full-time employment and may rely more heavily on part-time or precarious work, limiting their ability to save for retirement. Immigrant women may have reduced access to pension plans due to interrupted work histories or time spent outside of the Canadian workforce. These compounded disadvantages result in even greater financial insecurity in later life for these groups of women.

Factors Behind the Pension Disparity

Several factors contribute to the gender pension gap, primarily related to differences in employment patterns and caregiving roles. Traditionally, women tend to earn lower wages than men, work fewer hours, and take more time off for caregiving duties. These earning disparities have a direct impact on retirement savings and pension contributions.

Intersectionality and the Pension Disparity: the Old Age Security (OAS) requires ten years of residency for any pension, and forty years for the full benefit, disadvantaging newcomers. Although there is limited research on how the system affects marginalized groups, labour market data shows that factors like gender, race, and immigrant status intersect to influence workforce participation. Notably, marriage and motherhood significantly reduce full-time employment for immigrant women, in comparison to Indigenous and Canadian-born women, affecting their pension contributions and retirement security.

Childbearing and Caregiving: Women are more likely than men to leave the workforce, temporarily or permanently, after having children. In 2015, the employment rate for women with children under six years old was 69.5%, whereas it was significantly higher at 90.8% for men with children in the same age group. This difference limits women’s ability to contribute to pension plans. Additionally, women often take on most caregiving responsibilities, which can lead to part-time work. In 2021, 24.4% of female workers in Canada were employed part-time, compared to just 13% of their male counterparts, with childcare being the most frequently mentioned reason.

Unpaid Domestic Labour: Women also perform the bulk of unpaid domestic work. In 2017, 89.9% of mothers took maternity or parental leave at reduced income levels,

while only 11.9% of fathers took similar leaves. This reinforces long-standing gendered norms, further widening the pension gap.

Gender Wage Gap: The gender wage gap in Canada remains a significant factor contributing to the GPG. Two of the three pillars of the pension system—CPP/QPP and private retirement savings—are earnings-based, meaning that individuals who earn less over their careers will receive lower retirement benefits. In 2021, the average earnings difference between men and women in Canada was 28%. This gap in earnings throughout their careers leads to smaller contributions to pension plans for women, resulting in lower retirement incomes than their male counterparts.

The Structure of Canada’s Pension System

Canada’s pension framework consists of three primary components: Old Age Security (OAS) and the Guaranteed Income Supplement (GIS), the Canada Pension Plan (CPP) or Quebec Pension Plan (QPP), and private retirement savings.

Pillar One: OAS/GIS: The Old Age Security (OAS) and Guaranteed Income Supplement (GIS) are social pensions administered by the government. As these benefits are based on age and income rather than employment history, they tend to favour women with lower incomes and longer life expectancies. However, this pillar alone is insufficient to close the overall pension gap.

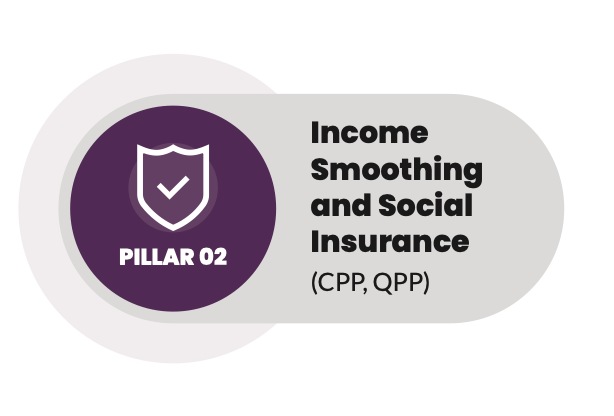

Pillar Two: CPP/QPP: The Canada Pension Plan (CPP) and Québec Pension Plan (QPP) are contributory pension schemes based on individuals’ earnings and contributions over their working lives. Because women typically earn less and may have gaps in their employment due to caregiving, they contribute less to CPP/QPP, resulting in lower benefits during retirement.

Pillar Three: Private Retirement Savings: Private retirement income, which includes workplace pension plans and personal savings like Registered Retirement Savings Plans (RRSPs), also shows disparities. Many women find themselves in part-time or lower-wage positions that often do not include pension benefits, making it challenging to save for retirement through personal plans. In fact, around 75% of adults in Canada lack access to workplace pension plans, with women facing a greater impact from this coverage gap.

The Path Ahead

Closing the gender pension gap demands a comprehensive strategy. Policymakers need to implement reforms that tackle the systemic challenges women encounter in their careers. Enhancing access to workplace pension plans, expanding eligibility for part-time employees, and providing incentives for employers to promote women’s retirement savings are important steps forward. Additionally, addressing systemic barriers for newcomers and individuals with intersectional identities is crucial. This could include reforming residency requirements for pension eligibility and creating targeted policies that support the unique challenges faced by women of colour, Indigenous women, and immigrant women in the labour market, ensuring fairer outcomes for all.

Furthermore, changes to the CPP/QPP could help reduce the gender pension gap. For example, providing caregivers with pension credits during periods of unpaid caregiving could help ensure

that time spent out of the workforce does not significantly affect women’s retirement income. Although Canada’s pension system is recognized as one of the best in the world, there remains

the need to tackle the ongoing gender disparities. With an increasing number of women nearing retirement, it is vital to secure fair pension outcomes to enhance gender equality and

ensure financial stability for all Canadians as they age.